KIP-76 introduced the Futarchy-Based Governance Rule for PNK Minting.

The KIP-81 proposal, currently live for voting and futarchy evaluation, expands the futarchy test to also apply to all proposals requesting DAO funding:

The current proposal, which establishes an ETH Treasury, carries the risk of attracting actors seeking to extract value through low-quality funding proposals. To mitigate this, we propose extending the Futarchy test from KIP-76 to all proposals requesting DAO funding.

We propose that the TWAP window for the futarchy test, as it applies to both KIP-76 and potentially (if approved) to KIP-81, be modified to measure the TWAP over the last 7-days of the voting period, to read as follows:

–

The Futarchy Test is considered passed for a KIP if the liquidity threshold is maintained for at least 7 days before the end of the KIP’s voting period, there is no modification to the wording of the KIP for the last 7 days, and the time-weighted average price (TWAP) of the “pass” (yes) outcome over the final 7 days before the end of the KIP’s voting period is greater than or equal to that of the “fail” (no) outcome. If not, the proposal fails the futarchy test, regardless of the Kleros DAO vote result.

–

Justification: the current 24h window seems insufficient for tokenholders to trade accordingly, making it technically challenging for tokenholders in favor of a proposal to coordinate to either buy YES-PNK, or sell NO-PNK, or alternatively, for tokenholders against a proposal to coordinate to sell YES-PNK, or to buy NO-PNK.

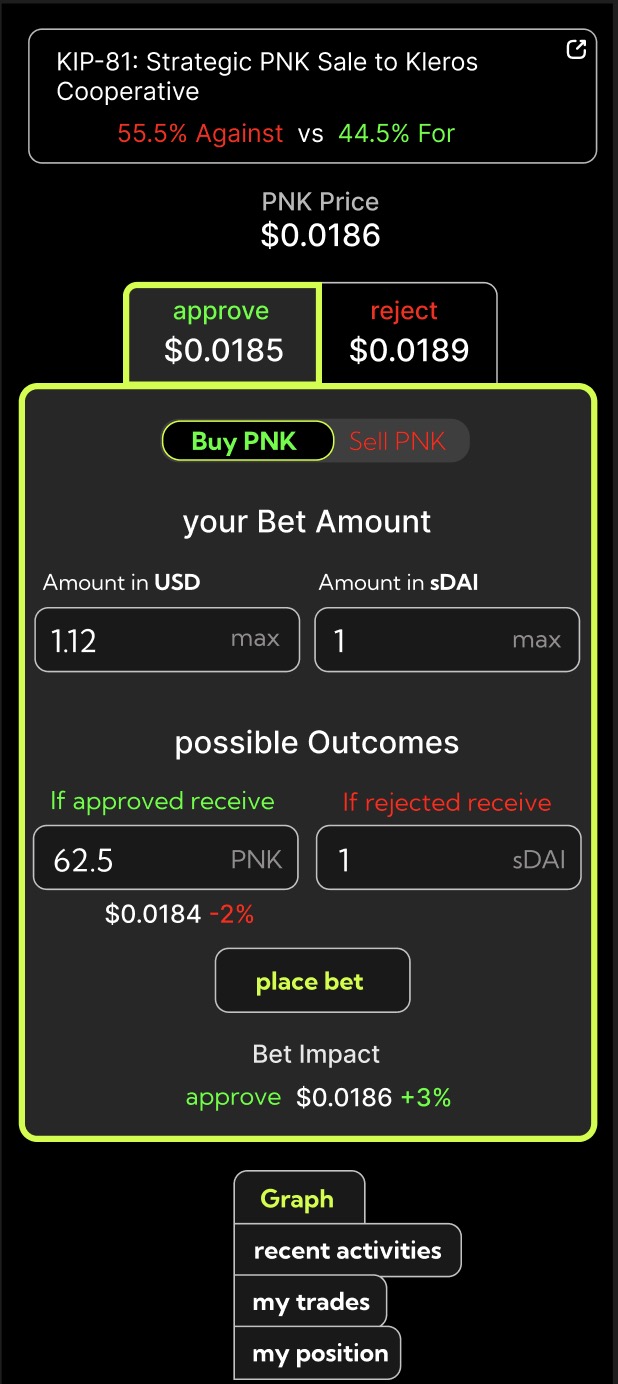

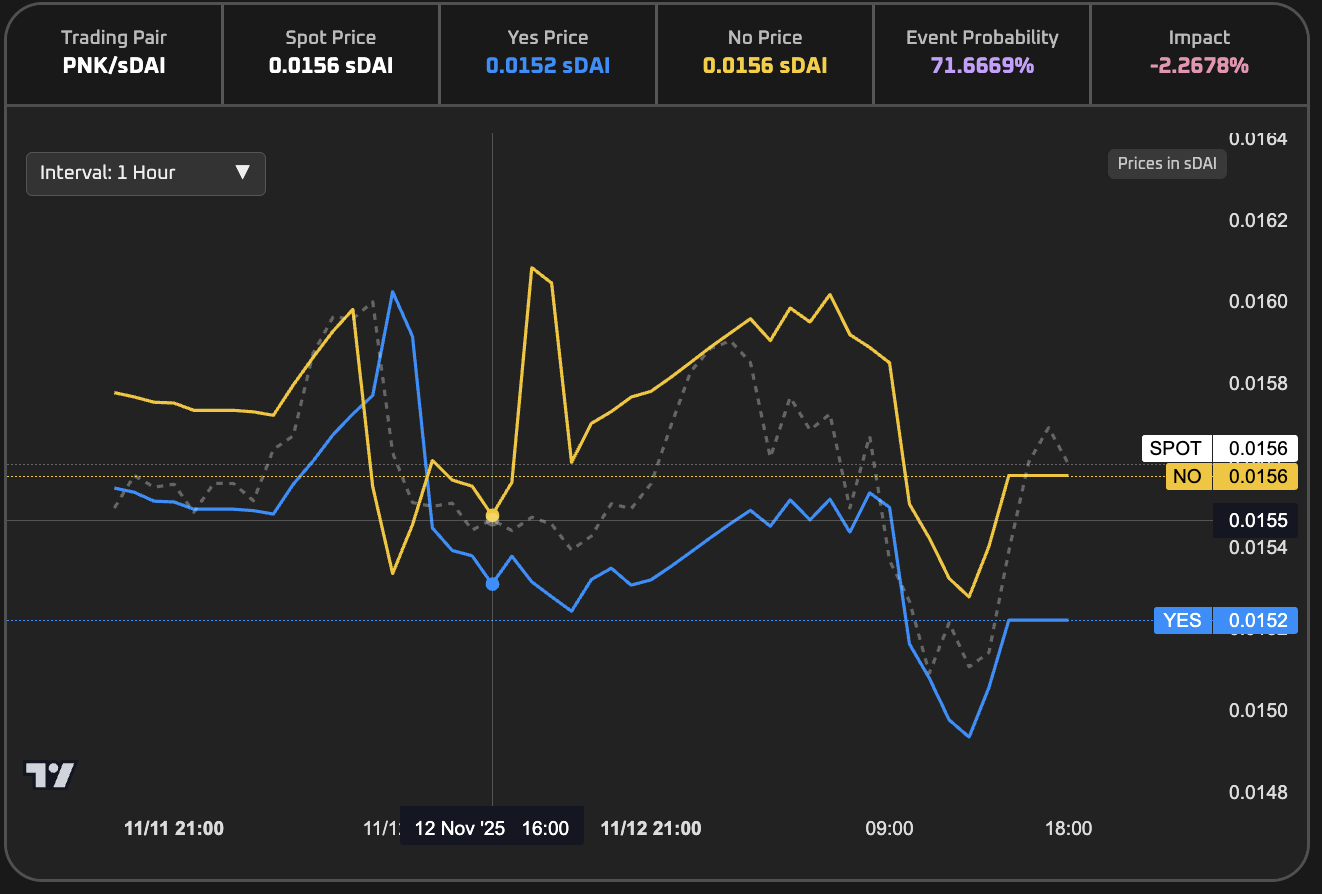

This difficulty can lead to fears or expectations of of market manipulation. In the current (pending) KIP-81, the futarchy markets currently estimate, in the first 1.5 days of the voting period, that the proposal will have a negative impact of -2%. If maintained until the end of the voting period, this will lead to the rejection of the proposal. And yet, the prediction market estimates (>70%) of the proposal passing, which means that the market estimate this impact estimate to “flip” at some point before the current date and the end of the voting period.

Such “predictable flipping” in a market is unusual, and means either that current markets are quite inefficient, or that there is an expectation of (successful) market manipulation of the conditional markets in the final 24h.

To reduce any fears that conditional markets are not accurate estimates of the token price post-decision, we propose to increase the TWAP window, making the estimate more robust.